CEO Michelle L. Jacko‘s article, “Legal and Regulatory Considerations for Going Independent,” has been published as an industry white paper in conjunction with Charles Schwab & Co., Inc.

The article outlines in 12 steps key factors for RIA’s who are considering going independent. “Advisors face legal and regulatory considerations when they decide to go independent. This report helps guide advisors through the labyrinth of issues involved in this decision.” Click here to read the article in PDF format or continue reading below.

Navigating the complex web of SEC and state registration requirements can quickly become overwhelming when you are trying to launch an independent practice. To ensure your Form ADV and other critical documents are accurate, timely, and fully compliant, consider utilizing our Regulatory Filings and Registrations services. Outsourcing this heavy lifting allows you to avoid costly regulatory missteps and frees up your valuable time to focus on what matters most—building your new business and serving your clients.

Introduction

This industry report is designed to help investment advisors assess the independent registered investment advisor (RIA) model and weigh the legal and regulatory considerations involved in going independent. This report is not intended to provide specific advice or advocate one advisory model over another. As with any new venture, you should consider consulting with industry experts and legal counsel for your particular business needs and circumstances.

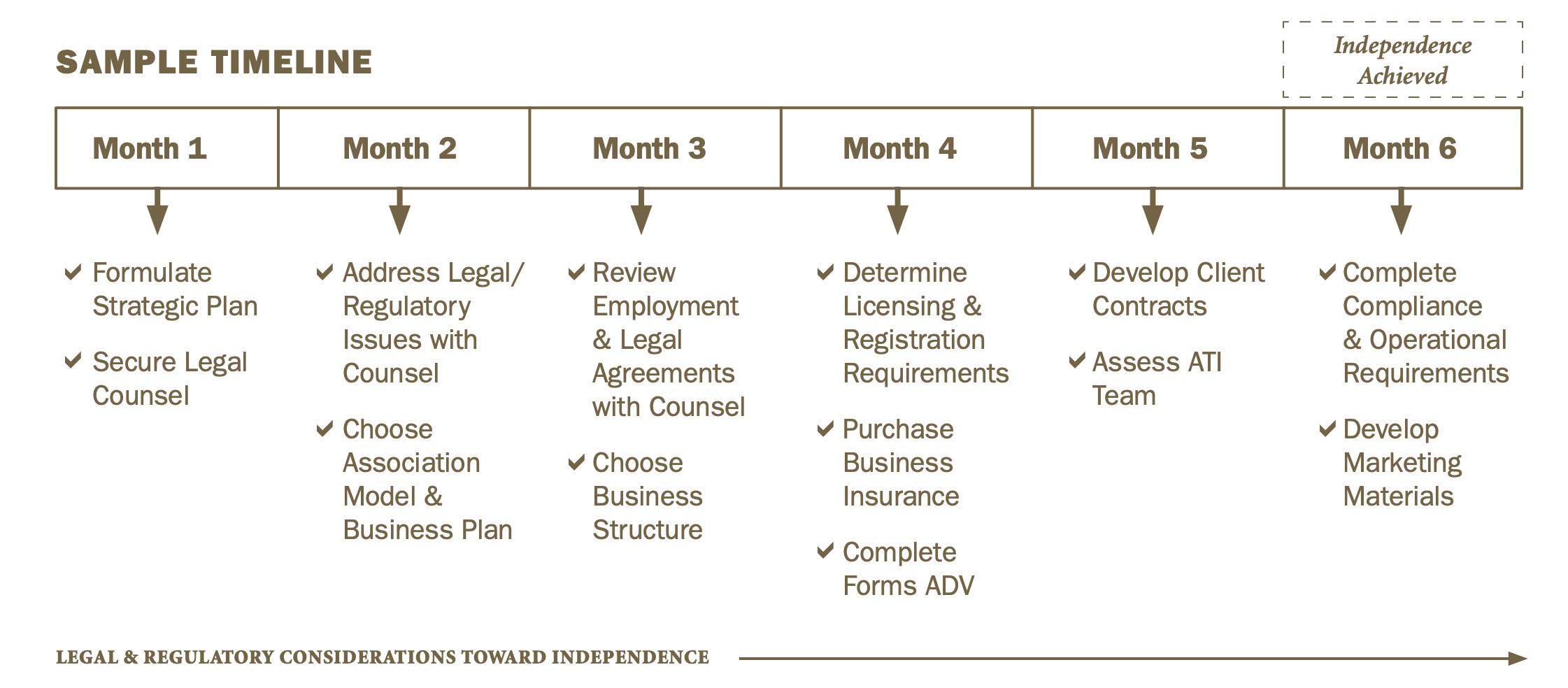

Advisors face legal and regulatory considerations when they decide to go independent. This report helps guide advisors through the labyrinth of issues involved in this decision. Typically, advisors take about six months to transition to the fully independent model. In some cases, advisors may be able to accomplish this transition in as little as two months. In others, it may take as long as 12 months. It all depends on the complexity of your business model and your unique circumstances.

This report helps advisors understand the legal and regulatory considerations of a transition and how long it takes to complete each step of the transition. It also provides specific questions to ask legal counsel, and directs advisors to additional resources.

While all of this can seem daunting, bear in mind that many RIAs have successfully managed these same challenges. By taking advantage of help from experienced attorneys and compliance-outsourcing options, and by following well-defined procedures, you can successfully make the transition to independence.

PART I: Formulate a Strategic Plan

Going Independent: Building Your Strategic Vision

Selecting the business model for your advisory practice is one of the most important decisions you will make as an advisor. Going independent means just that—independently running an advisory practice. From your products and services offered to your business cards and marketing materials, the choice is yours, allowing you more freedom—and responsibility—than you have working for a wirehouse or even an independent broker-dealer.

The first step is to build a strategic plan that charts your vision. Do you want to be completely independent, or would you prefer to have some help? If you require help, what type of assistance is most important to you? What types of products or services do you want to offer?

To help answer many of these questions, begin by considering what type of products or services you wish to offer clients. Then assess your market and define your offering. Finally, determine your business goals and expectations.

Is Independence the Right Choice for Me? Evaluating Benefits and Challenges

Independence comes with several benefits. You can:

-

Set your own course with limited potential conflicts

-

Act on new opportunities that allow your business to become more profitable

-

Set your own schedule

-

Select your own money managers

-

Diversify your client base

-

Offer a host of sophisticated products and services

Despite the benefits and potential success that come with independence, there are also a number of sometimes overlooked challenges. First, you will need to come up with your own marketing plan to obtain clients. A marketing plan is of paramount importance in the independent advisor marketplace. As the number of high-net-worth individuals has increased, so too has the number of independent advisors. To compete successfully for clients, you should make creating your marketing plan a priority.

Second, you will need to create a management strategy, which includes targeting clients, recruiting staff, and contemplating your long-term goals, including a succession plan.

Finally, you will need to build strong internal controls to comply with complex federal regulations. Since the securities industry arguably has the most rules and regulations, compliance with those requirements is complex and expensive. Undoubtedly, one of the top challenges facing new independent advisors is staying abreast of the latest regulatory rules and compliance requirements. Therefore, it is important to seek legal and compliance advice at the outset.

Decide What Type of Products and Services to Offer Clients

Independent advisors offer three main types of products and services: fee-based, commission-based and hybrid fee-and-commission–based approaches.

Fee-based products and services. Fee-based advisors are compensated only through their clients and not through outside sources. This approach allows you to work closely with your clients to customize services with limited conflicts.

Commission-based products and services. Commission-based advisors are compensated through the financial products they sell to clients. When the product is sold, the advisor typically receives a one-time commission and potentially recurring revenue (“trailers”).

Hybrid fee-and-commission–based products and services. Hybrid fee-and-commission–based advisors attempt to combine the positive product and service features of both models to ensure maximum efficiency. The hybrid advisor’s flexibility allows access to virtually unlimited investment products and resources, from securities to mutual funds to insurance products.

Assess Your Market and Define Your Offering

Once you have determined the types of products and services you want to focus on, it becomes easier to assess your market. Yet many of the products and services you offer likely depend on your existing clients’ needs. You may first wish to define which types of client best fit your business model, considering their ages, net worth and investment needs. Next, consider whether you want to offer additional services, such as family office,¹ financial planning or other host services.²

Identify Your Business Goals and Earning Expectations

Identifying goals and earning expectations enables independent advisors to solidify a plan that outlines their objectives. First, you must differentiate your practice from those of your competitors. Second, you must create goals and expectations that represent your definition of a successful independent firm. Your definition of success should focus on a single, clear vision. Too many competing visions will make success difficult to achieve. By taking a quantifiable approach to your strategic plan, you can determine benchmarks for measuring your success and advancing your goals and expectations.

Key Questions for Developing Your Strategic Plan

-

Have I determined whether I want a fee-based, commission-based or hybrid platform? Do I know what types of products and services I want to offer? Have I assessed my market and defined my offering?

-

Have I adequately assessed my financial goals and earning expectations? Are they documented in my strategic plan?

¹ Family office is defined as an office that manages all aspects of a family’s business, including expenses, tax compliance, aircraft and other transportation services, golf outings and investments.

² Host services may include tax planning, estate planning, insurance and similar services.

PART 2: Factors to Consider When Securing Legal Counsel

Once you have formulated a strategic plan, the next step is to secure legal counsel. Many types of attorneys are available. But bear in mind that specialists in one area may not be experienced in another. Therefore, it is essential to take time to research, interview and assess the skills and competence of the legal counsel you select.

When to Hire Legal Counsel

Consider hiring your legal counsel while you are still employed by or associated with your current employer. Your legal counsel will perform many different tasks, a few of which should be completed while you still are employed by a wirehouse or associated with your independent broker-dealer. For example, legal counsel will review and assess:

-

Your current employment or independent-contractor agreements

-

Your client contracts or agreements

-

Custodial relationships and the best techniques for transitioning clients

Legal counsel will provide guidance on the restrictive covenants, if any, that exist in these agreements and relationships. In addition, legal counsel will give you an overview of regulatory considerations and processes for compliance with industry rules, such as the Investment Advisers Act of 1940. Your counsel should provide skilled guidance on:

-

Licensing and registration requirements

-

Necessary books and records

-

Requisite written policies and procedures

-

Vital contracts and forms preparation

-

Marketing and advertising parameters

What to Expect of Legal Counsel

It is the role of legal counsel to provide guidance on the applicability of legal and compliance requirements for your advisory model. As an independent investment advisor, you will be subject to the Investment Advisers Act of 1940. These rules cover, among other things:

-

Application for Registration of Investment Adviser (Rule 203-1)

-

Eligibility for Commission Registration (Rule 203A-1)

-

Investment Adviser Registration with States (Rule 203A-4)

-

Books and Records to Be Maintained (Rule 204-2)

-

Written Disclosure Statements (Rule 204-3)

-

Advertisements by Investment Advisers (Rule 206[4]-1)

-

Custody or Possession of Funds or Securities of Clients (Rule 206[4]-2)

-

Cash Payments for Client Solicitations (Rule 206[4]-3)

-

Compliance Program Rule (Rule 206[4]-7) (for Federal registrants)

For additional investment advisor rules and regulations, please visit the Securities Exchange Commission (SEC) Web site at www.sec.gov.

Your legal counsel also should provide services and advice in the following areas:

-

Registration with the SEC or states

-

Contract and legal-agreement reviews and preparation

-

Mergers and acquisitions

-

Mock SEC and other regulatory examinations

-

Conflicts-of-interest evaluation

-

Authoring of disclosure documents (Form ADV Part II, Offering Documents, etc.)

-

Preparation of written policies and procedures

All of these tasks as performed are covered by a privileged and confidential relationship, known as the attorney-client privilege.¹ The attorney work-product doctrine² will apply when your outside legal counsel delivers the above services to you.

What to Consider When Selecting Legal Counsel

The attorney should fully understand the compliance and operational business requirements for advisors—not just those that pertain to the model an advisor will use. In other words, you should choose your attorney for his or her knowledge and understanding of the Investment Advisers Act of 1940 and all of the rules and regulations promulgated thereunder.

Always check with client references to ensure that the counsel you select:

-

Understands challenges you might face and the applicable laws that govern them

-

Clearly communicates the law firm’s billing practices and description of services to be provided

-

Assists in formulating a realistic strategy with insight and resourcefulness

-

Provides candid information about the benefits and costs of particular stages of your transition process, so you can prepare accordingly

-

Thoroughly understands the goals behind your business plan and acts according to that understanding

-

Uses time efficiently and provides detailed and informative analysis

-

Prepares a project plan keyed to the important phases of your transition³

In the initial meetings you should discuss the management and strategy of your transition. You should expect counsel to be candid and forthright. After counsel is engaged, he or she should explain how he or she evaluates the challenges you might face during the transition and detail the necessary tasks, their estimated time frame and the probable cost of what needs to be done. Please refer to Part 3 for a detailed discussion of the most common scenarios you may encounter.

Key Questions for Securing Legal Counsel

-

Before meeting with counsel, have I obtained copies of my employment contract or independent contractor agreement? Are there any other legal agreements that counsel should review, such as a sample client agreement?

-

Have I interviewed more than one attorney? Have I conducted reference checks, including background checks through the state bar, to ensure the individual is competent and experienced in all areas of advice?

Suggested Readings

Visit www.schwabinstitutional.com/public and go to “Considering going independent?”; click on “Get started,” then “Plan your new advisory firm,” and scroll down to “Legal and Compliance.”

¹ The attorney-client privilege protects confidential communications between an attorney and his or her client “made for the purpose of furnishing or obtaining professional legal advice and assistance” in anticipation of actual or anticipated litigation. See In re LTV Securities Litigation, 89 F.R.D. 595, 600 (N.D. Tex. 1981).

² “The work-product doctrine is an independent source of immunity from discovery, separate and distinct from the attorney-client privilege.” In re Grand Jury, 106 F.R.D. 255, 257 (D.N.R. 1985). It is broader than the attorney-client privilege to encompass the defense of administrative and other federal investigations. See In re Sealed Case, 676 F.2d 793 (D.C. Cir. 1982) (applying the doctrine to documents created by counsel rendering legal advice in connection with SEC and IRS investigations).

³ These phases include registration and licensing, preparation of contracts and written policies and procedures designed specifically for your business model, investment surveillance and technology solutions, and training and guidance on advertising standards and portability of performance numbers.

PART 3: Legal Counsel’s Role in Addressing Legal and Regulatory Issues

Your legal counsel serves as your advisor through the transition process. Just as you would not consider driving your new Mercedes off the dealer’s lot without sufficient insurance, you should not consider investing in and building your independent practice without expert advice. Your legal counsel serves as your mentor, guiding you through the preparation, development and execution phases that lie ahead.

Now that you have selected your legal counsel, we will take an in-depth look at counsel’s role in your transition plan.

Provides Advice on Business Plan

Your legal counsel is a crucial advisor to your new business plan. An experienced legal counsel has most likely handled business plans similar to yours and is proficient in setting up new, fully independent advisory businesses. Your counsel will be able to help identify gaps or conflicts in your plan. In addition, he or she will provide advice regarding safeguards and protections you might not have considered. When you meet your counsel, be sure that you bring:

-

Concept business plan

-

Target market information

-

Financial goals and expectations

Be prepared to discuss your business plan concepts and your rationale for the market you’ve identified. Based on this information and your financial goals and expectations, your legal counsel will propose a business structure addressing your specific needs.

Formulates a Business Structure

Your legal counsel will be familiar with different business structures that will be best for you and your business. Once you discuss your business plan strategy, your legal counsel will recommend how to structure your business for productivity, prosperity and protection. Possible business structures are discussed in Part 6. Be prepared to discuss these issues with your counsel:

-

Partners

-

Officers and directors

-

Profit sharing and stock issuance

-

Private vs. public entities

-

Responsibilities of principals

Along with your accountant and other industry consultants, your legal counsel will be one of your best assets in formulating your business’s structure legally and for maximum protection.

Provides Counsel on Regulatory Requirements

Myriad state and federal securities laws, rules and regulations govern the investment advisory industry. You are stepping into a maze of rules and regulations that you were not necessarily familiar with while working for an established broker-dealer, bank or trust company. Your legal counsel should be familiar with the rules and regulations that dictate the way you will do business in this new realm. Look for outside legal counsel experienced in:

-

The Investment Advisers Act of 1940

-

State securities laws

-

SEC and state firm and individual registrations

Additionally, be sure to ask your counsel pointed questions to ensure he or she understands your operational model.

Reviews Legal Agreements with Current Employer

The review of your existing legal agreements with your current employer could be the most important part of your legal counsel’s work at the outset. Your legal counsel will assess all legal agreements with your current firm, looking for, among other things:

-

Non-compete language

-

Non-solicitation language

-

Any other restrictive language

Because you probably signed various contracts and agreements with your current employer, you will need to rely on your legal counsel to advise you on your rights under those contracts and agreements. Your legal counsel should be very familiar with these types of contracts and restrictive clauses to advise you on what you can and cannot do when you leave your firm. Remember, this part of your breakaway will have lasting effects on your new business and the business you may pursue once you have separated from your firm.

Reviews and Drafts New Client Agreements

Most business law attorneys can assist you in determining a proper legal structure for your new firm. They also typically have expertise in contract law and the preparation of business contracts. Since you will select an attorney who specializes in investment advisor formation, he or she can assist you in drafting advisory contracts and investment policy statements for your clients. Try to provide as much information about your business strategy as you can at the outset of your relationship. This will enable your legal counsel to draft exacting client agreements for your use.

Provides Registration with Regulatory Agencies

Registration procedures for investment advisors now are completed online via NASD’s registration platform. Both the SEC and state regulators require that all registration forms be filed through their central registration depository (CRD) and Investment Advisory Registration Depository (IARD). With the assistance of counsel, newly formed investment advisors must complete and submit the following forms for regulatory approval before transacting any advisory business:

-

Form ADV Parts I and II

-

Form U-5 (from your former firm)

-

Form U-4 (on behalf of your new business, if applicable)

Additionally, some states may require you to complete your written policies, procedures and client advisory agreements when you submit your registration. Your legal counsel will help you determine what is required for your registration. For more detailed information about the licensing and registration process, please refer to Part 7.

Form ADV Part I is the application form used by investment advisors to register with the SEC and state regulators. It comes as a questionnaire format and includes information related to your:

-

Client base

-

Assets under management

-

Financial industry activities and affiliations

-

Participation or interest in client transactions

It also inquires into any disciplinary history of the advisor and related persons.

Form ADV Part II serves as your “client brochure.” It provides your current and prospective clients with detailed information about your advisory services, fees, and actual and potential conflicts of interest you have identified. You will need to include detailed information on your business, including:

-

Services and fees

-

Participation or interest in client transactions (code of ethics policies)

-

Investment or brokerage discretion

-

Additional compensation

-

Other business activities

Through interviews with key personnel and discussions on your business strategy, legal counsel will prepare a draft of Form ADV Parts I and II for your review and approval. Allow plenty of time for redrafts and amendments as you fine-tune your business plan. The electronic submission of Form ADV Part I will initiate your application to be an investment advisor.

Develops Policies and Procedures

A key component of any investment advisory firm is a compliance program. Rule 206(4)-7 of the Investment Advisers Act of 1940 states that federally registered investment advisors must have “written policies and procedures that are reasonably designed to prevent violation of federal securities laws.”¹ Therefore, if you register with the SEC, you must have written policies and procedures. If you register with state regulators, written policies and procedures may not be mandated. But keep in mind that your firm will be required to show evidence of internal controls during examinations, which means that you must document your firm’s processes.

The SEC has provided much guidance on its expectations in this area. A firm’s policies and procedures must be real, reflect the type of business you engage in and define the internal controls you have enacted. Prepackaged manuals will not suffice during a regulatory examination. Your legal counsel will need to know as much about your business as possible so that he or she can customize your written policies and procedures and provide guidance on internal controls.

Timelines and Costs Associated with Legal Engagement

The costs for legal engagement vary widely among firms, sometimes based on the region of the United States where the law firm is located. Because you are seeking legal counsel with specialized experience, you may expect the costs to be more than if you simply hired a general legal practitioner. Keep in mind that a generalist may not know the finer points of this specialized area of practice. For that reason, what you save in hourly rates may be wasted on the amount of time it takes a general practitioner to become familiar with investment advisory laws.

Most practitioners charge an hourly rate. Rates generally are based upon the experience of the attorney or paralegal working on your matter. Paralegals will have the least expensive hourly rate, while senior partners will have the most expensive billable rate. Attorneys may charge a flat fee depending on the project or type of service provided. This is common for legal services related to business-structure formation (LLCs, S corporations, etc.) and registering new investment advisors.

Timing is essential for getting your business off the ground. You should hire legal counsel before separating from your current business, so you can identify challenges that may arise once you give notice, and so you can minimize downtime in getting your new business venture started.

The registration process for state-registered advisors typically takes 30 to 90 days from the initial date of the filing. SEC filings generally take less time for processing. Discuss with your counsel whether you are eligible to rely on the Newly Formed Adviser Rule,² which provides a 120-day grace period after SEC approval to get your assets under management up to the $30 million required to be an SEC-registered investment advisor.

Finalizing your business-entity paperwork takes about one month from the date you file it. For more information on related expenses, please refer to Part 6.

Key Questions for Starting Work with Legal Counsel

-

Before meeting with legal counsel, have I assessed my resources in terms of time, commitment and revenue to devote to the transition?

-

Do I have a projected timeline and budget for accomplishing the transition?

-

Is counsel skilled in all areas where I need help, including registration, business formation, policy and procedure development, and client agreements?

Suggested Readings

Visit www.schwabinstitutional.com/public. Go to “Considering going independent?” Select “Go with the leader” and click on “Plan.”

¹ Investment Advisers Act of 1940 (“Advisers Act”), Rule 206(4)-7 and Investment Company Act of 1940 (“Company Act”), Rule 38a-1(a)(3).

² For additional information, please refer to the Investment Advisers Act of 1940.

PART 4: Choose an Association Model and Finalize a Business Plan

The next step of your transition process is to meet with your counsel to determine which model is the best fit for your business. There are generally three types of business models: full affiliation, supervised independence and full independence.

Full Affiliation: The Wirehouse Model

The full-affiliation advisor generally works for a wirehouse, broker-dealer, bank or trust firm as an employee of the parent company. The reputation of the parent company provides the advisor with instant credibility through his or her affiliation. In addition, the employee is supplied with an office, necessary equipment, research services, investment choices, operational and compliance assistance, a mentor (or branch manager) and an assigned team. Because the employer bears these expenses, payouts are generally between 30 and 45 percent.¹

The parent usually owns the client relationship and enters into an employment contract with the advisor. Most agreements specify provisions relating to non-competes with, and non-solicitations opposed to, the parent company in the event the employee wishes to terminate his or her advisory relationship. While at first this may appear to be customary and acceptable, you should be aware of the challenges you will face if the parent company believes you are competing for its clients. If such competition occurs, it is likely that the parent company will obtain a temporary restraining order (TRO) against you. This could potentially tarnish your professional reputation and negatively affect your income and bottom line. Before you enter into any non-compete agreements with a parent firm, seek guidance from your counsel.

Supervised Independence: Independent Broker-Dealer Model

The supervised independence model appeals to those who seek to share expenses with the broker-dealer while retaining some independence in managing their practices. Typically, the advisor will affiliate with an independent broker-dealer or insurance company as an independent contractor. This allows the advisor more freedom, particularly with regard to “owning” the client relationship. At the same time, the advisor is provided with a supervisory framework. The independent broker-dealer (IBD) will have detailed policies, procedures and processes the advisor must follow during the affiliation. The IBD is responsible for supervising all activities of its independent contractors. As a result, the IBD will require the advisor to, among other things:

-

Submit his or her business model, including any outside business activities, for review and approval by the IBD

-

Submit for review all client information, including new account forms, trades and transactions for client accounts

-

Submit for review and approval all marketing, advertising and sales literature materials

-

Undergo periodic examination of the advisor’s books and records

-

Comply with the IBD’s supervisory policies and procedures or risk having the affiliation terminated

The supervised independence model allows both commission-based and fee-based compensation. Depending on the gross dealer concessions (GDCs) achieved, the advisor’s payout typically ranges between 80 and 92 percent.² The payout is based on the percentage of revenue earned minus a percentage to the IBD for supervisory and other support services received. However, the percentage to the IBD is much less than in the full-affiliation model, because the IBD provides less support than a wirehouse.

Full Independence: Registered Investment Advisor Model

The fully independent model gives advisors the most freedom. Rather than being employees or independent contractors, fully independent advisors are self-employed. They set their own standards and autonomously control all expenses associated with the business. One of the most appealing features of this model is that the advisor owns 100 percent of the revenue for all services performed. There is no payout to a third party—just standard fees associated with custodial, trading and other services.

The fully independent financial advisor typically formulates a registered investment advisor (RIA) from which all business is conducted. Through the RIA, you select the products and services that best meet the unique needs of your clients. You are free to select and implement any business model and advisory platform, as long as they comply with state and federal rules and regulations.

As a new independent advisor, you will need to:

-

Determine the management fee to be charged. Typically, advisors choose to charge a fee based on a percentage of a client’s total portfolio (about 80 to 150 basis points per year). Alternatively, the advisor may charge an hourly or flat fee.

-

Select the law firm, company or individual to register the RIA. RIAs are independently registered either with the SEC or their state securities regulator. The registration process may be complex, so it is best to have a trustworthy specialist undertake it.

-

Select a custodian, broker-dealer or bank. The advisor will need to determine who is responsible for holding client assets, executing and settling trades, and providing other required products, services and expertise to the RIA (unless otherwise directed by the client).

-

Designate a chief compliance officer responsible for ongoing legal and compliance support. If the advisor is registered with the SEC, the RIA will need to designate the firm’s chief compliance officer, who is responsible for administering the RIA’s compliance program. If the advisor is a state registrant, the RIA will need to decide who will be responsible for ongoing legal and compliance support. Options include:

-

Doing it yourself

-

Outsourcing it to legal counsel or a compliance consultant

-

Combining the two

-

The fully independent model will allow you to earn more than you can as an employee, but many additional expenses are associated with it. On one hand, you will be able to build equity in a profitable business that you can eventually pass on to your family, transition to a business partner or sell. On the other hand, as an independent, you are fully liable and accountable for all advisory activities conducted. You will no longer have the supervisory structure of a parent company. Instead, you will develop your own policies, procedures and processes and be responsible for all regulatory compliance requirements. With total independence comes full responsibility.

Selecting your custodian is a very important decision for an independent advisor. While the custodian may not be directly involved in the RIA’s day-to-day business decisions, the custodian can provide guidance and resources to help develop internal operations.

Key Questions for Choosing an Association Model

-

Do I want to be an employee or run my own business?

-

What level of support and liability shielding do I want from an affiliation?

-

Have I been asked to sign a non-compete agreement with the employer?

Suggested Readings

Visit www.schwabinstitutional.com/public, click “Considering going independent?” and then “Why go independent?” Also in this section, click “A recent report” to read Going Independent: Why Many Successful Financial Advisors Are Starting or Joining Independent Firms by Moss Adams LLP and Schwab Institutional (2007).

¹ For more information about the spectrum of independence, please refer to the article Going Independent: Why Many Successful Financial Advisors Are Starting or Joining Independent Firms, by Moss Adams LLP and Schwab Institutional (2007).

² Payout percentages referenced reflect typical historical industry benchmarks for the independent contractor model.

PART 5: Review Current Employment or Independent Contractor Legal Agreement and Prepare for Transition

Before transitioning, it is important to have your counsel review employment and other agreements for specific limitations so you can avoid problems in the future.

Common Limitations and Contractual Clauses Outlined in Legal Agreements

Advisors who have written legal agreements with their existing firm may have particular restrictions that affect their ability to transition easily to the independent model. Common limitations and contractual clauses include:

-

Privacy policies and confidentiality provisions

-

Non-compete agreements

-

Non-solicitation clauses

-

Compensation terms

Let’s briefly review each of these common limitations.

Privacy issues. Many parent firms have detailed privacy policies that prevent advisors from taking confidential client information with them. In addition, certain federal regulations prohibit the use of confidential client information. Before copying down any client Social Security numbers or account numbers, be sure to ask your counsel for specific guidance on prohibited and acceptable practices.

Privacy policies frequently are detailed either in a separate section of your employment agreement or incorporated in a confidentiality agreement. Confidentiality agreements are one of the most common types of restrictive covenants. A typical confidentiality covenant restricts current and former employees from using or disclosing the employer’s confidential and proprietary information provided during the course of employment. Confidentiality agreements are enforced by most states, as long as the restrictions list specific categories of information that are truly confidential, proprietary and not publicly known.

Non-competes. Most frequently a non-compete clause will prohibit an advisor from competing with the wirehouse or parent firm. Non-compete agreements or clauses may be legal and binding, depending on state or local laws, the scope of the restrictions provided and the terms by which you leave employment.

Typically, a non-compete clause is enforceable as long as it:

-

Is reasonable in scope (e.g., geographically limiting or for a limited period of time)

-

Is necessary to protect the interest of the firm

-

Does not seriously restrict your ability to make a living

On the other hand, in states such as California,¹ non-compete agreements generally are not legal unless someone sells a business or dissolves a partnership and agrees not to compete with the new owner.² Such agreements may also be legal when necessary to protect a trade secret,³ which moreover, has been deemed to apply to misappropriation of client lists not readily available to competitors through general sources.⁴ Typically, however, the California courts have held that employers cannot restrict the livelihood of current or former employees. Your legal counsel can provide you with the specifics in your area.

The enforceability of a non-compete also depends on whether some sort of consideration was paid for signing the agreement. While new employment alone might be viewed as sufficient compensation, if you were asked to sign the non-compete after becoming employed, the court may hold that ongoing employment is not compensation enough.

Since the enforceability of a non-compete is based on myriad facts and circumstances, it is essential to see an attorney before deciding to go independent. This will help you avoid conflicts down the line, particularly once you give your employer notice. If the non-compete is reasonable in scope and generally enforceable by your state, it is likely that the non-compete will be honored in court should you breach its provisions. However, under certain circumstances the non-compete may not be enforceable. For example:

-

The advisor quits because the employer asks him or her to conduct illegal activities

-

The employer breaches the advisor’s employment agreement

-

The employer is based in a different state than the advisor, who operates in a state that does not enforce the non-compete

If you are planning to give notice and have signed a non-compete agreement, try your best to leave on good terms. Often this will help eliminate fears of retaliation on both sides and result in a professional, ethical departure. Having an attorney help you plan the notice process may stave off potential legal actions down the road.

Non-solicitation clauses. Non-solicitation clauses generally are less restrictive than non-compete agreements. Such clauses specifically prohibit the advisor from calling on, soliciting or taking clients away from the parent firm for a particular period of time after an employment agreement ends. As with non-compete agreements, the enforceability of a non-solicitation clause depends upon the jurisdiction, facts and circumstances. Your legal counsel can help you avoid legal conflicts.

Compensation terms. Depending on the type of legal agreement entered into, compensation terms will differ. For the fully affiliated advisor with an employment contract, compensation will be tied to the advisor’s production, based on revenues generated from clients. The employer generally also offers additional forms of compensation, including health and life insurance and, in the wirehouse model, bonus payouts for long-term service.

On the IBD side, compensation also is based on the advisor’s production. However, benefits received by employees, such as insurance or a 401(k) plan, typically are not offered as compensation to independent contractors. These benefits may be available to IBD advisors for a fee and are offered as value-added options. Additionally, to further compete with the fully affiliated model, the supervised independent model frequently offers other benefits, such as equity ownership.

Once you give notice to the parent firm, benefits associated with your affiliation frequently are lost. For instance, if you receive stock options for joining a particular wirehouse or IBD that is planning to go public in two years, you may lose that option once you give notice of separation to the parent firm. Advisors should review the compensation terms in all legal agreements carefully with their counsel before providing notice to the parent. This allows advisors to evaluate economics before making the transition.

Factors to Consider for a Successful Transition

Creating a timeline. When speaking with counsel about your strategy plans and your employment or independent contractor agreements, be sure to discuss timing issues in your practice. For some, a transition in December (or at a fiscal year end) or in mid-April or October (during tax season) might negatively affect service to clients. Taking these critical times into account, develop a transition calendar. With the help of your counsel, decide when and how to:

-

Handle client data before resigning (i.e., what data, if any, is non-trade-secret information)

-

Notify clients of your transition

-

Select a custodian

-

Transition client accounts

Avoiding temporary restraining orders. It is critical to work with counsel to resolve legal issues early so you can avoid negative legal consequences later. One of the most common protections used by parent companies is the temporary restraining order (TRO). TROs forbid an action or threatened action by a defendant. TROs are granted without notice or hearing and require the defendant to cease and desist from an action, thereby preserving the status quo until a hearing can be had to determine the propriety of any permanent injunctive relief. TROs typically are granted to employers who allege that a former employee has solicited employees away from the parent or is using confidential client account data to the detriment of the parent.

Certain wirehouse employers have very specific restrictive covenants. One such firm states in part within its employment agreement, “In the event I breach any of the covenants … I agree that (parent) will be entitled to injunctive relief. I recognize that (parent) will suffer immediate and irreparable harm and … therefore consent to the issuance of a TRO ordering that I (1) return all records…, (2) for one year I am enjoined and restrained from soliciting any account… [and] (3) for one year I am enjoined and restrained from accepting any accounts that were solicited in violation of this employment agreement.”

The agreement goes on to define the restraints on solicitation, including call-ins, write-ins and transfers, among other things. Therefore, before you resign and transition client accounts, be prepared to defend against any restraining orders or breach of restrictive covenant claims. Review your employment agreements very carefully with legal counsel. Your attorney will help you avoid a TRO and potential legal defense costs.

After you resign, be prepared to show the parent company:

-

Any announcements (as defined by the NASD and SEC) sent to clients

-

Written statements from clients stating that you have not solicited them for their business

-

Any other proof showing that you did not solicit the parent firm’s clients

Such proof of non-solicitation often reveals groundless claims and results in a release from further legal actions from the parent. Remember, while your current association may have required you to sign this agreement as a condition of your employment, the law allows you to practice your profession. You are allowed to prepare to compete and can even create an independent practice while still employed. You may not, however, compete with existing contract obligations. Seek help from your counsel to point you in the proper direction.

Selecting the right custodian. Just as important as selecting your legal counsel is picking the right custodian for your business. It is essential to develop a strong relationship with your custodian and utilize its transition services. Many custodians, such as Schwab Institutional, have a dedicated conversion team to help transfer your clients’ assets. Advisors typically receive technology solutions and are assigned to a custodial relationship manager who works to understand the advisor’s needs and support the transition.

Your custodial conversion team will:

-

Help coordinate your conversion project plan

-

Serve as liaison between you and the custodian’s internal departments

-

Monitor progress of new account openings and transfers of accounts

Key Questions for Reviewing Current Agreements and Preparing for Transition

-

Have I had my counsel review:

-

My current employment agreement or independent contractor agreement?

-

Any privacy policies or confidentiality agreements provided to me by the parent firm?

-

Any legal agreement containing my compensation terms, including benefits such as stock accumulation grants and deferred compensation agreements?

-

Stock option plans and related legal agreements?

-

-

Do I have any time constraints (such as tax season) that should be factored into my transition timeline?

-

Have I selected my custodian? How will outside counsel, the custodian and I work together to maximize efficiencies?

Suggested Readings

-

Jacobson, William A., “Escaping Non-Solicitation Agreements,” Registered Rep (August 2001).

-

Morrison & Forester Legal Updates & News Bulletins, “How Far Can Employers Go to Protect Their Trade Secrets and Other Proprietary Information?” (April 2004).

¹ California Business and Professions Code Section 16600 (“Section 16600”) provides “ … every contract by which anyone is restrained from engaging in a lawful profession, trade, or business of any kind is to that extent void.” This notion is reinforced by two recent California Court of Appeal decisions, Thompson v. Impaxx, Inc., 113 Cal. App. 4th 1425, 1428 (2003), and D’Sa v. Playhut, Inc., 85 Cal. App. 4th 927, 934 (2000).

² California Business and Professions Code §§ 16601, 16602.

³ Metro Traffic Control, Inc. v. Shadow Traffic Network, 22 Cal. App. 4th 853, 859 (1994); Muggill v. Reuben H. Donnelley Corp., 62 Cal. 2d 239, 242 (1965).

⁴ See MAI Systems Corp. v. Peak Computer, Inc., 991 F.2d 511, 521 (1993); Morlife, Inc. v. Perry, 56 Cal. App. 4th 1514 (1997); American Paper and Packaging Products., Inc. v. Kirgan, 183 Cal. App. 3d 1318, 1325 (1986).

PART 6: Choose Your Business Structure

There are many ways to establish a business structure. Independent investment advisors must know the advantages, disadvantages, expenses and liabilities that come with each structure before selecting one. Forming your business organization is the most crucial preliminary step in your transition to the independent model.

Sole Proprietorship

A sole proprietorship is a business entity that has no legal separation from its owner. All debts and liability incurred by the sole proprietorship are the owner’s. While there are no corporate taxes, the sole proprietor pays all taxes on profits through his or her personal income taxes. Sole proprietors generally register their business entity under a trade name.

Advantages: There are several distinct advantages to the sole proprietorship. First, since there is only one owner, decisions can be made quickly. As a general rule, sole proprietorships encounter the fewest governmental regulations of any business entity. A sole proprietor may also dissolve the entity with relative ease. Tax preparations are simpler for a sole proprietor because they are included on the owner’s income taxes. Lastly, all profits earned in a sole proprietorship go directly to the owner.

Disadvantages: The principal disadvantage of a sole proprietorship is its unlimited liability. If the company is sued, the owner may be personally responsible. Raising capital also can be difficult because shares of the company cannot be sold to third parties. In addition, sole proprietors are responsible for their own health insurance and other benefits. Moreover, if the owner dies, the entity ceases to exist.

Expenses: Generally, the only associated expense with creating and maintaining a sole proprietorship is payment for rights to a trade name.

Corporation

A corporation is a business entity owned by individual members or other legal bodies or both. A corporation is recognized as a separate body distinct from its individual members. Generally, the individual members share ownership in the corporation through stock. The four characteristics of a corporation are:

-

Limited liability to the extent of assets

-

Continuity of life

-

Centralization of management

-

Free transferability of ownership interests

Advantages: The primary advantage of a corporation is the limited liability it creates for its members. Since the law recognizes a corporation as essentially its own person, any lawsuits that arise are directed at the entity. The only losses that can be incurred by the members of the corporation are any contributions they have made or paid for in shares of stock. This greatly reduces losses for a potential investor. Limited liability makes raising capital easier.

Corporations and their assets also have a perpetual lifetime. This enables the entity to outlive its members. Therefore, investors do not have the threat that the corporation and its value will suddenly dissolve. This ensures stability, creating an incentive for long-term investment transactions.

Disadvantages: The primary disadvantage to a corporation is its taxation. As a general rule, the government taxes the profits of a corporation. The remaining profits are distributed to the shareholders in the form of dividends. These dividends are then taxed again by the government. Corporations require more time than any other form of organization. They are heavily regulated by the government and require dedicated resources for maintaining and filing corporate records.

Expenses: A corporation is the most expensive kind of organization to create. Every corporation must register to assume limited liability. Upon registration, a corporation must designate a principal address and a registered agent. The registered agent is a person or business that receives legal service of process. Thereafter, the corporation is required to file articles of incorporation. The articles describe the general nature of the corporation, the amount of stock it is authorized to issue, and the names and addresses of the directors. Registration and the filing of the articles of incorporation require fees and payments, which vary depending on the jurisdiction and type of corporation established (e.g., S corp, C corp, etc.). It is highly recommended that you consult your counsel before forming your corporation.

Partnership

A partnership allows partners to share in the profits or losses incurred in their business undertakings. Partners maintain a joint ownership in the entity relative to their share in the business.

Advantages: Partnerships are favored for their tax advantages. Unlike corporations, partnerships do not incur a dividend tax. This means the owners of a partnership are taxed on their profits only once. Plus, taxes are easy to file because they come directly from the owners’ income tax statements.

Partnerships are relatively easy to set up. The partnership requires only an agreement between the parties that outlines each partner’s responsibilities. Moreover, since there is more than one owner, raising capital in a partnership is easier than raising capital in a sole proprietorship.

Disadvantages: The most significant disadvantage to a partnership is the liability that each partner assumes. Each partner is jointly and personally liable for the actions of the other partners. Furthermore, all of the profits made in the partnership must be shared. Partners may disagree about payments and overall decision making. Some states may have registration requirements for certain styles of partnership, so be sure to consult with your legal counsel. Lastly, partnerships, like sole proprietorships, can be easily dissolved, making long-term investments difficult.

Expenses: Partnerships are inexpensive to create since they require only a contract between the partners. Because the law attaches the business to the individuals involved, there is generally no registration requirement. Some states may impose registration requirements in limited circumstances.

Limited Liability Company

A limited liability company (LLC), is a blend between a corporation and a sole proprietorship. LLCs were created to give members the limited liability assumed in a corporation with the tax advantages of a sole proprietorship or partnership. However, it is more complex to form an LLC than a general partnership.

Advantages: The LLC is most typically advantageous to a small business. Its hybrid nature gives small business owners limited liability while also giving members certain tax advantages. LLCs also are easily convertible to corporations, so a growing company can switch fairly easily from LLC to corporation.

LLCs do not require an annual board meeting among shareholders. Each member has a specified share in the company and relative decision-making power. LLCs, like corporations, are enduring entities and may be structured so they do not terminate upon the death or withdrawal of a member. LLCs also are advantageous from a taxation standpoint. They allow members to choose how to be taxed—as a sole proprietor or as a corporation.

Disadvantages: Many states, including Alabama, California, Kentucky, New Jersey, New York, Pennsylvania, Tennessee and Texas, levy a franchise tax on LLCs. This tax is essentially a fee imposed by the state in consideration for the limited liability the LLC assumes. Raising capital can be challenging for LLCs because investors generally are more comfortable investing in a corporation. Moreover, in some states, LLCs do not require an operating agreement among their members. Those who operate without such an agreement can run into problems.

Expenses: An LLC may be expensive to create. If a desired LLC has more than two of the four characteristics of a corporation described above, corporation forms must be used in the creation process.

Limited Liability Partnership

A limited liability partnership (LLP) has characteristics of a partnership and a corporation. An LLP is made up of individual partners, but each can assume limited liability.

Advantages: An LLP gives partners the tax advantages of a partnership while ensuring limited liability. The LLP is particularly useful in professional settings where each partner will take a managerial position.

Disadvantages: Depending on the jurisdiction, the creation of LLPs is limited to certain professions, such as law, architecture and accounting. Moreover, since the partners generally all have a managerial stake in the organization, disagreements can arise.

Expenses: The expenses of creating an LLP are comparable to those of creating an LLC. Since an LLP limits liability, the partners must often use corporation forms in the creation process. This increases the time and money required.

Key Questions for Choosing Your Business Structure

-

What is my primary objective in formulating my business structure? What is most important to me:

-

Limit of personal liability?

-

Taxation concerns?

-

Number of governmental regulations?

-

Filing and registration costs?

-

Ease of dissolution?

-

Continuity of life?

-

-

Do I need to raise capital for my business?

-

Is there a budget limit to establishing my business structure?

Suggested Readings

Visit www.schwabinstitutional.com/public, click “Considering going independent?” and then click “What are your options?” Also on www.schwabinstitutional.com/public, click on “Plan your new advisory firm” to read the Schwab Institutional MKT report Business Planning: Building a Road Map for a Profitable Future (2001) and to use the Schwab Institutional “Go Independent Planning Tool.”

PART 7: Determine Type of Licensing and Registration Required

Seek advice from your legal counsel on the various business plans available before you register your investment advisory business. Registration is complex, and an industry expert can help you navigate it.

Once you have formulated your strategic plan, secured legal counsel, addressed potential legal and regulatory issues, finalized your business plan, reviewed legal agreements and established your business structure, you are ready to determine the licensing and registration requirements of your new business model. This step in your transition toward independence marks the halfway point. Once you reach this point, the process should move rather quickly.

Registering as an Independent Registered Investment Advisor

Registration with authorities. If you are going to transition to either the fully independent model or to an IBD model that permits you to have your own RIA, you will need to register. Depending on your assets under management (AUM), your business entity will need to register either in the states where your clients reside or with the SEC to conduct advisory business. As part of the registration process, you will need to complete and submit Form ADV Part I to apply with the SEC or states. You will also need to provide notice filings to applicable states. Simultaneously, you will need to create and perhaps deliver to the appropriate regulatory body your Form ADV Part II (or client brochure). For more information on the application process, visit the SEC Web site at www.sec.gov.

-

SEC registration. The SEC provides detailed guidance on when an investment advisory firm must register with the federal government. Review the SEC’s registration requirements and considerations (see sidebar) with your legal counsel.

SEC Registration Requirements

You may register with the SEC if you have (AUM) of at least $25 million but less than $30 million. However, you must register with the SEC if your AUM are $30 million or more. Currently, if you are a state-registered advisor and you report on your annual updating amendment that your AUM increased to $25 million or more, you may register with the SEC. If your AUM increased to $30 million or more, you must register with the SEC within 90 days after you file that annual updating amendment.

Exemptions. Subject to various exemptions, advisors may also register with the SEC if they are:

-

An advisor to an investment company

-

A nationally recognized statistical rating organization

-

A pension consultant

-

An affiliated advisor (i.e., you control, are controlled by, or are under common control with an investment advisor registered with the SEC, and you have the same principal office and place of business as that other investment advisor)

-

A multi-state advisor (you are required to register as an investment advisor with the securities authorities of 30 or more states)

-

An Internet investment advisor

If you do not have AUM of $25 million or more on the date that you register but believe you will have that amount or more within 120 days of the date that the SEC approves your registration, you may register under the “Newly-Formed Adviser” exemption, which can be found under SEC Rule 203A-2(d). If you find that you do not have the AUM to remain an SEC-registered investment advisor after the 120 days have elapsed, you must withdraw from the SEC registration and register as a state investment advisor.

To start the registration process, the SEC requires you to file Form ADV Part I online through the IARD system. You are not required to file Form ADV Part II with the SEC; however, you must keep a copy in your files and deliver a copy of Form ADV Part II (client brochure) with material disclosure information to all of your existing and prospective clients. Once you have filed your Form ADV Part I with the SEC, you will need to file notice electronically with all states where you will be doing business.

There are associated fees for filing notice in each state, as well as a filing fee to register with the SEC. For more information about these registration fees, please visit the IARD Web site at www.iard.com/fees.asp.

-

State registration. If you have assets under management of $25 million or less, your business entity will need to register with each state where you conduct investment advisory business (typically, where your client resides). Each state has the authority to enact laws that govern the conduct of investment advisors and their businesses. During the registration process, state regulators will want detailed information about you and will want to gain a solid understanding of what you will be doing as an investment advisor. Each state has rules regarding registration processes for Form ADV filings and licensing of individuals and has regulatory requirements for conducting your advisory business. While state regulations are similar to the federal rules promulgated and enforced by the SEC, each state has its own idiosyncrasies, and you will need to review the requirements for each state fully before filing your application.

It is important for you (or your counsel) to build a relationship with state regulators. This will help you to gain a better understanding of the state’s expectations and create an open dialogue about any questions or concerns the state may have about your advisory business model. During the registration process, the state may:

-

Require that you register online using the Investment Adviser Registration Depository (IARD) to file your Form ADV Part I

-

Request a copy of your Form ADV Part II and attachments via email

-

Ask for copies of your client agreement forms and other contracts that you will use with your clients

-

Review Form ADV Part I online and provide notice if your registration is accepted

-

Provide notice if state regulators need more information

-

Provide notice of registration via U.S. Postal Service

Partnering with an Existing RIA

If becoming fully independent is not attractive to you, consider partnering with an established RIA firm or associating with an IBD until you are ready for total independence.

Join an established RIA firm. There are many pros to joining an established RIA firm. For one, you will not have to worry about the time, resources and expenses associated with the rigorous RIA application process. Because you join an already-formed business structure, you will not have to search for offices, supplies or support staff. Moreover, rather than paying all expenses out of your own pocket, you will be able to share overhead and business expenses. This also is a good model for advisors who desire a mentor or do not necessarily want to run their own business.

However, you need to be aware of some of the concerns associated with this structure. You may encounter certain conflicts between you and the existing principals, including:

-

Differing styles and value systems

-

Competition for resources

-

Incompatible business models (this may happen after you join the firm)

You will need to determine how your needs and goals compare with those of the established firm before you decide to join an existing RIA.

Associate with an independent broker-dealer. By associating with an IBD, you will be able to take advantage of many value-added services while retaining a degree of independence. As discussed in Part 4, an IBD has a compliance division, which is ultimately responsible for supervising your activities. Compliance staff can give you support and guidance on many things, including:

-

Regulatory requirements for sales transactions and advisory services

-

Exception reports for trading activities

-

Licensing and registration requirements for your advisory firm

-

Advertising and marketing reviews

This model is helpful because it offers guidance on compliance and operational requirements without the need to create the infrastructure on your own. However, it is also limiting in that the IBD has the authority to disapprove your business model, forbid certain sales activities and charge additional overrides for these services. As your business model changes and you wish to diversify into a more complex service structure, the IBD may not be able to support you, which may restrict your advisory platform offerings. Therefore, when evaluating whether or not to partner with an existing RIA, base your decisions on your desired business plan and service offerings, both now and in the next several years.

Obtaining Necessary Licenses to Perform Services

The types of services you offer, along with the state you are based in, determine what licenses you need to conduct business as an RIA. For those advisors who need to be dually licensed with both the National Association of Securities Dealers (NASD) for brokerage services and the SEC or states for advisory services, the number of securities licenses required increases.

Register for licensing examinations. If you wish to offer advisory services, most states require you to successfully complete the Series 65 examination. As an alternative, if you have a Series 7 license through the NASD, you can take the Series 66 examination (which covers both the Series 65 advisory rules and Series 63 blue sky regulations).

In addition, some states offer an exemption for those individuals who: a) were grandfathered into registration based on previous examinations and experience, or b) have a professional designation, such as ChFC, CFA or CFP.

Although the investment advisor examinations are administered through the NASD, they are governed in accordance with state law and registration requirements. You may wish to take this exam while you are still with your current employer, especially if your employer is an NASD member firm, which helps to expedite the process. If you are not associated with an NASD member firm, you can apply for the exam by filing a Form U10. For more information and for a copy of the Form U10, visit the SEC Web site, www.sec.gov. For NASD information, go to www.nasd.com. In addition, be sure to review your state’s rules and regulations to determine whether you qualify for an exemption.

PART 8: Purchase Business Insurance

In today’s litigious environment, there is a growing tendency to include anyone and everyone involved in alleged wrongdoing in a client transaction. This is why financial advisors should obtain professional liability and errors and omissions (E&O) insurance policies to cover them against: a) claims and related expenses; and b) the costs of legal defense against allegations of breach (including material errors), fraud or misappropriation of client funds.

Errors & Omissions Coverage

E&O insurance covers damages incurred by a client resulting from the advisor’s error or omission. Contrary to common belief, general liability insurance does not cover lawsuits resulting from errors or omissions. It is important that you obtain and maintain E&O coverage to protect yourself against such potential consequences and to limit your financial exposure.

Why Should Advisors Purchase E&O Insurance?

E&O policies cover legal defense costs for actions brought against you by a client seeking damages. Regardless of how groundless the client allegation, E&O insurance pays for any judgments against you, including court costs, defense costs and amount of an award up to your policy’s coverage limits.¹ E&O insurance extends worldwide and covers both W-2 employees and 1099 subcontractors. Having E&O insurance is like having property insurance: you are protecting yourself against the chance of a bad fire.

How Much Coverage Should I Get?

E&O insurance comes in increments of $1 million. Deductibles typically range from $1,000 to $25,000. Most E&O insurers require projected revenue of more than $1 million to remain eligible for coverage. The cost of E&O insurance is about $6,000 to $7,000 a year for a $1 million limit-of-liability policy, but costs can vary greatly, depending on the following factors:

-

Previous claims against the advisor

-

Types of products the advisor offers (mutual funds, alternative investments, private investment funds, etc.)

-

Whether you have discretionary client accounts

When purchasing E&O insurance, be aware of your policy’s exclusions. Check that the carrier you find covers everything your practice does. Then make sure the policy you select:

-

Has a high insurance rating

-

Has a “Duty to Defend,” not just “Right to Defend” clause, so the carrier will have to defend you in court

-

Is based on “Incident” so coverage begins as soon as an incident occurs (so you do not have to wait for a claim)

Is E&O Insurance Required?

Generally, E&O insurance is not required. However, as an independent advisor, you will be fully liable for any claims brought against you and your firm. Consider purchasing E&O insurance to limit your business risk.

Other Insurance Coverage

Depending on your business model, you may wish to consider the following types of insurance coverage.

Fidelity Bonds

Fidelity bonds, also known as blanket bonds, give brokerage firms protection against losses resulting from employee dishonesty. These obligations cover losses from theft, larceny, embezzlement, forgery, misappropriation, wrongful abstraction or willful misapplication. Although referred to as a fidelity “bond,” it is really an insurance policy.

You may also want to consider other forms of crime-insurance policies (burglary, fire, general theft, computer theft, disappearance, fraud, forgery, etc.) to protect the company against employee-dishonesty losses.

ERISA Bonds

The Employee Retirement Income Security Act of 1974 (ERISA) requires advisors who handle pension funds to have a fidelity bond. Bond limits are typically 10 percent of each plan’s assets and should not exceed $500,000 per plan. Fidelity bonds protect organizations from the effects of dishonest acts by:

-

Plan trustees and officers

-

Plan employees, administrators or managers (other than independent contractors)

-

Directors, trustees or employees who handle assets of pension plans insured by the policy

Surety Bonds

A surety bond is a contract between three parties: the principal, the obligee and the surety. As an independent investment advisor, you will have contractual obligations with your clients. In the fully independent business model, the advisor serves as a principal, and the client serves as the obligee. Surety bonds protect the independent advisor from a default or breach of any contractual obligation to the client or both. The amount covered through a surety bond is known as the penal sum. The penal sum is the maximum amount the surety will cover in the case of a default.

Directors and Officers Liability Insurance

Directors and officers (D&O) liability insurance protects the managing partners from lawsuits. In a world where the public is holding directors and officers more and more accountable for their decisions, D&O insurance is worth considering. D&O insurance policies cover issues including, but not limited to: investment management, release of nonpublic information, conflicts of interest and hiring-firing decisions.

Regardless of the type of insurance you buy, be sure to work with a reputable insurance professional to ensure you have appropriate coverage.

Key Questions about Business Insurance

-

Should I get E&O insurance? If yes, what should coverage amount be?

-

Have I conducted due diligence on the insurance carrier? Is it reputable?

-

What other types of insurance should I get, based on my business model? For example, am I required to get an ERISA bond?

¹ The carrier will require you to pay your deductible before paying your claim. 21 of 35

PART 9: Complete Form ADV and Other Disclosure Documents

To register as an investment advisor, you will need to complete Form ADV Parts I and II. Part I is filed electronically with the SEC and states through the IARD. This application provides identifying information about the firm, including how the firm is organized, its employees, client types, compensation arrangements, advisory activities and disciplinary disclosures.

Form ADV Part II, also referred to as the “client brochure,” is one of the most important documents to a fully independent advisor. Part II discloses to clients and prospects material information about the advisor’s services, fees, investment strategies, education standards and various conflicts of interest. Part II need not be filed electronically.

The Investment Advisers Act of 1940 requires all advisors to:

-

Deliver a copy of Part II to prospective clients

-

Offer annually a copy of Part II to all current clients

In addition, the advisor must maintain a current copy in his or her files and make it available to the SEC upon request.

As a new RIA, you should become familiar with the disclosures you must provide to clients, not only in Form ADV but also in new contracts, and marketing and sales materials, such as requests for proposals and website information. Work with your counsel to develop adequate disclosures relating to the areas discussed below and any actual or potential conflicts. Decide how you will create and adopt procedures to prevent and address these conflicts.

Understand Your Fiduciary Duty

Before you file your Form ADV, you should understand your role as an advisor and your fiduciary duty to your clients. All investment advisors are held to a fiduciary standard. This means that you must always act in your clients’ best interest, placing all client interests above your own. As an investment advisor fiduciary, you are held to a higher standard than you were in your brokerage relationships, which were based on suitability principles.

In its instructions for Form ADV, the SEC further clarifies the role of a fiduciary:

“[As a fiduciary, you] are required to make full disclosure to your clients of all material facts regarding conflicts of interest between you and your client. You therefore may have to disclose to clients information not specifically required by Part II of Form ADV.”¹

Consequently, the fiduciary standard requires disclosure of any actual or potential conflicts of interests to clients before or at the time of investing. Failure to provide sufficient disclosure is one of the leading deficiencies noted by the SEC during its examination process. Moreover, an advisor’s failure to disclose material conflicts could be deemed a violation of federal securities law and may result in fines, disciplinary actions and suspension.²

Let’s now consider the areas that you will need to evaluate with your counsel to formulate disclosures relating to your new business.

Identify Advisory Services and Fees

In this section of Form ADV, the advisor needs to identify what services are provided and by whom. For example, if services are provided in conjunction with another advisor, broker or third-party administrator, you must clearly state what services you do or do not provide. In addition, there should be sufficient detail relating to how information will be obtained from the client and the extent to which advice will (or will not) be tailored to the client’s specific circumstances. In addition, you will need to provide information relating to your advisory fees.

If you have performance-based fee accounts, you will need to describe:

-

The level of risk and related expenses associated with performance fees

-

How you are protecting against favoritism

-

Your method of calculating the fee

Disclose Other Business and Financial Activities

Depending on the kinds of services your business offers, you may need to disclose outside business or financial activities. For example, many advisors serve as insurance agents and provide insurance services to their clients. Other advisors may be affiliated with a broker-dealer through which client trades occur. These activities present a potential conflict of interest and must be disclosed.

Participation or Interest in Client Transactions—Code of Conduct

Conflicts of interest may exist whenever an advisor participates or has an interest in a client transaction. Most typically this occurs when an advisor:

-

Engages in a principal transaction³

-

Acts as a broker for the client

-

Conducts an agency cross-transaction⁴

-

Has other financial interests (such as selling affiliated funds)

-

Allows personal securities trading for its advisory personnel

Under Rule 204A-1 of the Investment Advisers Act of 1940, all investment advisors registered with the SEC⁵ are required to have a written Code of Ethics (Code). The Code generally contains the advisor’s policies and procedures as they relate to, among other things:

-

Personal trading

-

Gift giving or receiving

-

Insider trading

-

Ethical walls (i.e., screening procedures) and the potential that they may be insufficient to manage conflicts of interest

-

Outside employment or directorships and other business activities

-

Provisions for:

-

Complying with applicable Federal securities laws

-

Prompt reporting of Code violations to your chief compliance officer

-

Requiring supervised persons to provide written acknowledgment of their receipt of your Code

-

Federally registered investment advisors also are required to include a summary of the Code in Item 9 of Schedule F of Form ADV, as well as information on how a client or prospect can obtain a copy of the Code in its entirety.

Codes of Ethics typically are authored and/or reviewed by legal counsel. For more information on how to develop your Code of Ethics, contact Schwab Institutional for their Compliance Review Supplement: Best Practices for Investment Advisor Code of Ethics by the Investment Counsel Association of America (August 2004).

Disclose Investment and Brokerage Discretion